Optimising BESS Returns: Key Financial Metrics and Strategies

Here at VPP Partners we are always thinking about all things energy. The energy transition and all the moving parts are complex and looking for ways to demystify the challenges and help overcome them is one of our key drivers.

Recently, VPP Partners's Energy Specialist Lachlan Ryan built a model to answer a question that he had been toying with for some time. The question was along the lines of “There must be a way to create a graph that would show the required spread between charge and discharge for a BESS in the wholesale electricity market for different capital costs to meet a desired financial metric”.

It was believed that this would help to demonstrate a few different aspects relating to batteries in the NEM:

- Understanding Capex Requirements: Enabling the quick identification of the capex ranges required to get reasonable project returns based on expected charge and discharge prices.

- Highlighting Value Stacking: Highlighting that value stacking with other value streams is likely needed to meet the required financial returns.

- Value streams and contracting: Understanding your value streams and the potential importance of contracting your assets to firm up revenue.

- Trading capabilities: The requirement for competent trading capabilities to realise as much value as possible from the market.

Key Assumptions

The model itself had several assumptions that are highlighted as follow:

- Target internal rate of return (IRR): 12%, 15%, 18%

- Round trip efficiency (RTE): 85% (losses applied to charge cycle)

- Annual degradation rate: 3%

- Depth of discharge (DoD): 90%

- Cycles per day: 1.5

- Project duration: 15 years

- Interest rate: 0% (self-funded model)

The Challenge of Real-World Charging Prices

A critical assumption in this model is that the battery charges at $0/MWh, which means the spread is equal to the discharge price. However, in real-world scenarios, the battery won't always charge at $0/MWh, and due to the round-trip efficiency (RTE), the actual required spread isn’t straightforward.

For example:

- A 1MWh BESS charging at $0/MWh and discharging 0.85MWh (with 85% RTE) at $100/MWh results in a margin of $85/MWh.

- If the battery charges at $100/MWh and discharges at $200/MWh (maintaining a $100/MWh spread), the margin drops to $70/MWh.

- To achieve the same $85 margin, you would need to discharge at $217.6/MWh.

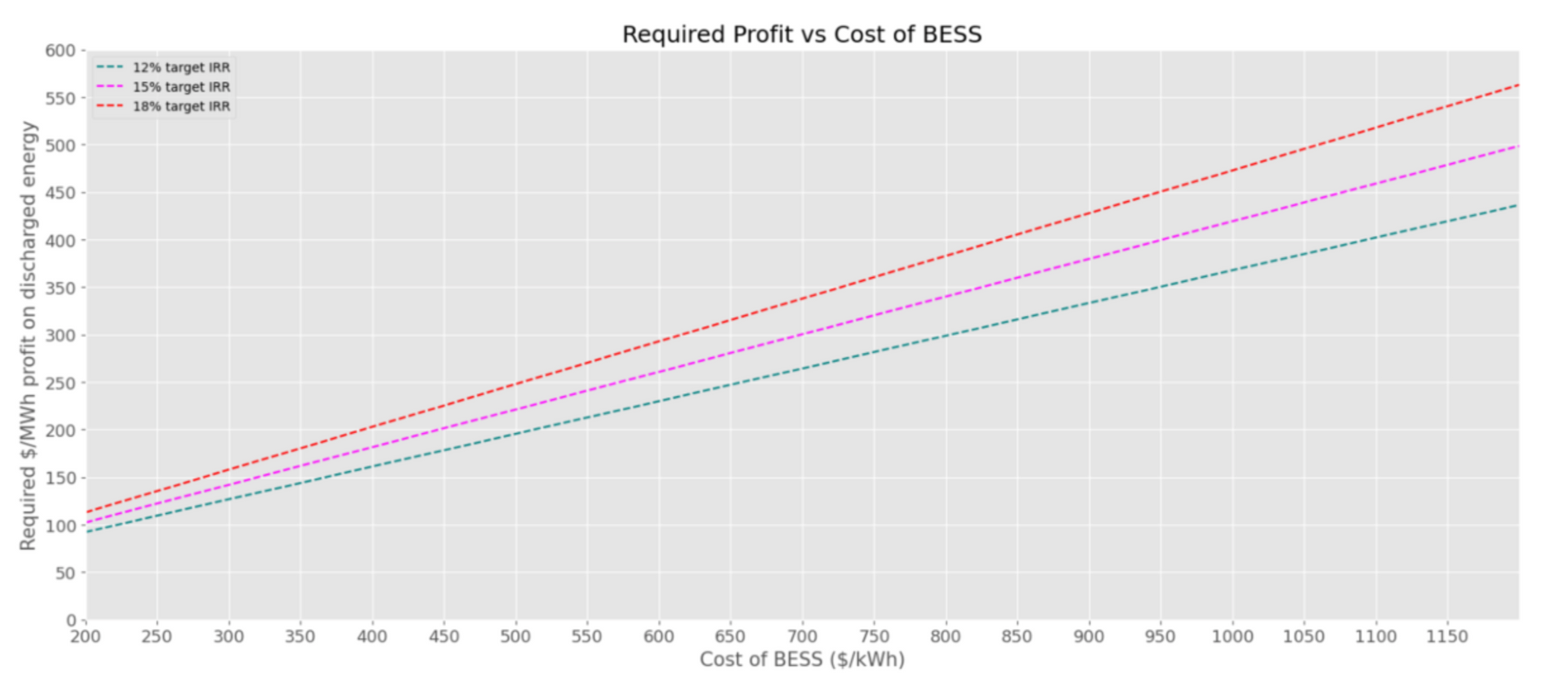

This led to a redefined the problem: Instead of calculating the required spread, the result was required profit per MWh for all discharged energy. This model created the graph ‘Required Profit vs Cost of BESS’, where the x-axis is the capital cost of the battery system, and the y-axis is the required $/MWh profit required for all the discharged energy.

Focusing in the 12% IRR line, it has the following linear equation:

Required $/MWh Profit = 0.34 × CAPEX + 23.45

So, for example a $700/kWh BESS (utility scale is regularly installed cheaper than this) needs a $261.5/MWh profit on all the discharged energy. If the BESS was to charge at $0/MWh, it would simply need to discharge at $261.5/MWh.

As noted before, charging at $0/MWh is very rarely the case. Due to the round-trip efficiency problem that was highlight, a formula was produced that enables us to determine the required charge and discharge price for a battery to meet a goal IRR for different capex values while handling the RTE.

Discharge Price = (Charge Price/0.85) + 0.34 × CAPEX + 23.45

Or rearranged to:

Charge Price = 0.85(Discharge Price − 0.34 × CAPEX − 23.45)

As an example, let’s say you were able to find a contract that was paying $300/MW for all capacity discharged during a certain time of the day, this would mean that to achieve a 12% IRR with a capex value of $700/kWh you would need to charge at $32.78/MWh.

Now the question is, ‘is this an achievable spread between charge and discharge?’ and the answer unfortunately is not that easy. Historical price analysis can be completed to see if there has been sufficient value in the market. However, as we all know historical market outcomes don’t necessarily demonstrate what future outcomes could be, especially in the currently rapidly evolving market. Developing your own forward view of the market when making any investment decision is crucial.

If as a developer, you are chasing IRRs like 15% and 18% obviously the price spread will need to be larger. To keep the spread in a range that is achievable in the market its crucial to keep capex as low as possible and have a trading strategy that can extract high value from the assets.

Conclusion

"The evolving landscape of BESS projects demands not just innovation, but strategic foresight. As we navigate these complexities, remember: 'Success in energy storage isn't just about capacity, it's about capability.'

In essence, the evolving landscape of BESS projects requires careful consideration of multiple value streams, robust financial planning, and creative contracting to bridge the gap between market realities and financial expectations.

If you are having issues in your projects between these two worlds, feel free to reach out to the team here to discuss this model further and how we can support you.

Share on...